China Solar Dominance: Global PV Supply Chain Impact

or complex compliance issues.

clearance and fund security.

ChinaThe industrys rapid expansion has garnered widespread global attention and is expected to significantly impactcomponent supply chains in the coming years.According to the latest report from Wood Mackenzie,how will this trend shape the future landscape of the global photovoltaic market?Below is an in-depth analysis of this issue.

I.Expansion of Chinas Photovoltaic Industry

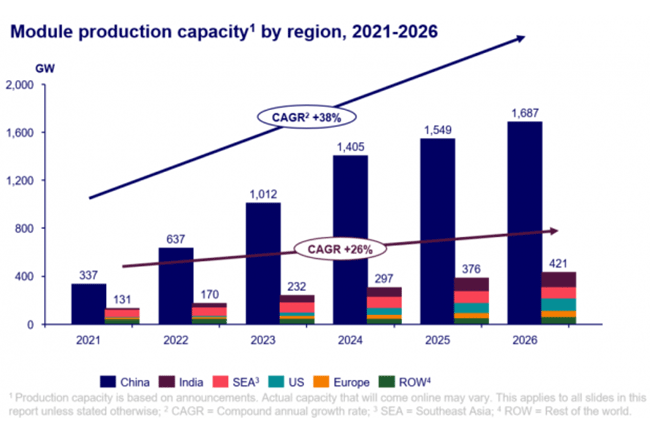

China is expected to invest more than $130 billion in its domestic solar industry between 2023 and 2026.It is predicted that by 2024,China will have a production capacity of over 1TW for silicon wafers,batteries,and components,sufficient to meet global annual demand from now until 2032.This expansion is primarily driven by the high profitability of polycrystalline silicon,technological upgrades,and policy support,enabling China to dominate the global solar supply chain and continuously widen the technological and cost gap with its competitors.

II.Impact on Global Supply Chains

Despite overseas governments efforts to promote local solar manufacturing growth,their costs remain uncompetitive compared to Chinese supply.Chinese-made modules are priced significantly lower than those from Europe and the U.S.Overseas markets like the U.S.and Europe,lacking key upstream raw material capacity,cannot compete with China on price for domestically produced modules.Additionally,while the U.S.Inflation Reduction Act and Indias Production-Linked Incentive scheme aim to expand module capacity,both countries will remain reliant on Chinese wafer and cell supplies in the short term.

III.Future Market Competition

The oversupply in the market and intense competition will characterize the future solar supply chain.The demand for P-type solar cell production lines is expected to decline starting from 2023,with demand falling to just 17% of supply by 2026,indicating the need for upgrades or gradual shutdowns.Additionally,the expansion of solar cell manufacturing capacity is expected to outpace that of silicon wafers and modules,making solar cells the most fiercely competitive segment of the module supply chain.Due to its robust incentive mechanisms,India is projected to become the world’s second-largest module production hub by 2025.

In summary,Chinas photovoltaic industry expansion will significantly impact global supply chains in the coming years.Chinese manufacturings price advantages and technological leadership will make it difficult for overseas markets to reduce reliance on Chinese wafers and cells.Simultaneously,market oversupply and technological upgrades will usher the photovoltaic industry into a more challenging era.

Was this helpful? Give us a like!

Contact our experts for compliance audits, precise quotes, and one-stop customs support.

Recent Comments (0) 0

Leave a Reply